A trust is a legal arrangement through which one person (or an institution, such as a bank or law firm), called a trustee, holds legal title to property for another person, called a beneficiary.

Trusts fall into two basic categories: testamentary and inter vivos.

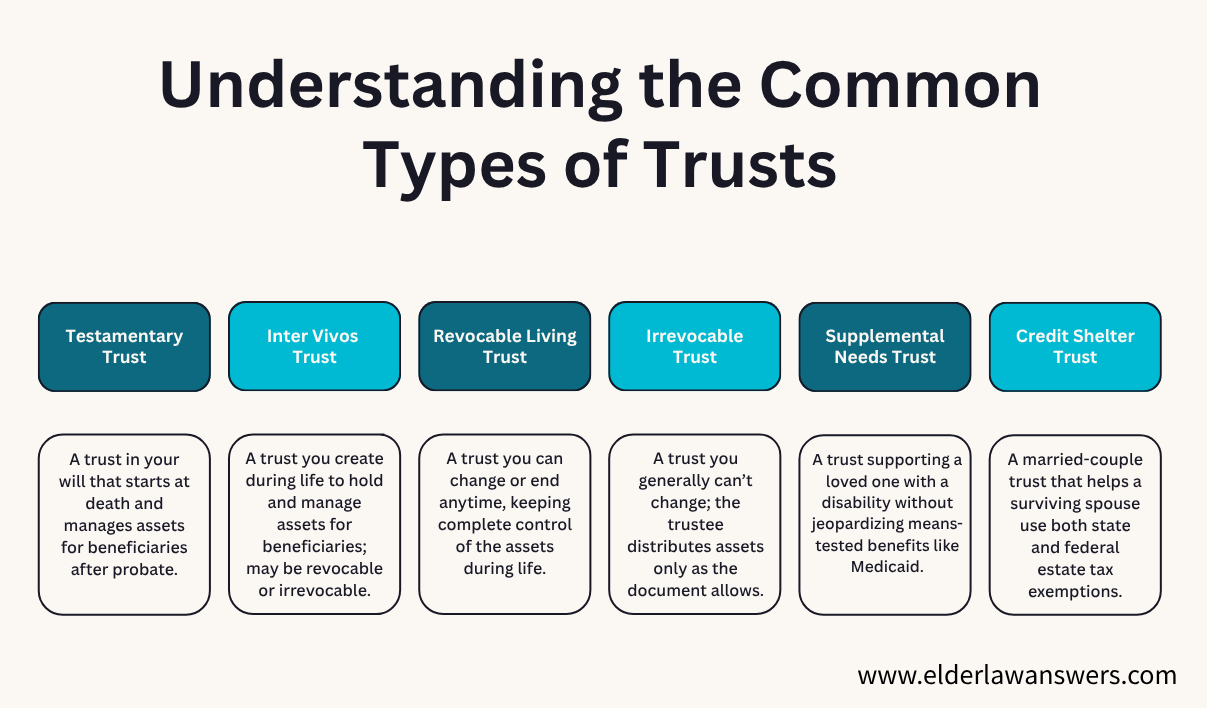

What Is a Testamentary Trust?

A testamentary trust is a trust created by your will. It does not become effective until you die.

What Is an Inter Vivos Trust?

In contrast, an inter vivos trust starts during your lifetime. In Latin, inter vivos means "between the living." You create an inter vivos trust now, and it exists while you are alive.

Inter vivos trusts may be revocable and irrevocable.

Revocable Trusts

Revocable trusts are often referred to as living trusts. With a revocable trust, the person who created the trust, called the grantor or donor, maintains complete control over the trust and may amend, revoke, or terminate it at any time. This means that if you are the grantor, you can take back the funds you put in the trust or change the terms of the trust. You can reap the benefits of the trust arrangement while maintaining the ability to change the trust at any time prior to death.

Revocable trusts are generally used for the following purposes:

- Managing and protecting assets: Revocable trusts permit the named trustee to administer and invest the trust property for the benefit of one or more beneficiaries.

- Avoiding probate: At the death of the trust grantor, the trust property passes to whoever is named in the trust. It does not come under the jurisdiction of the probate court, and its distribution need not be held up by the probate process. However, keep in mind that the property of a revocable trust will be included in the grantor's estate for tax purposes.

- Tax planning: Assets that you place in a revocable trust will be part of your taxable estate. However, you can work with an estate planner to draft the trust so that the assets will not be part of your beneficiaries’ estates. This can help their estates avoid taxes when they pass away.

Irrevocable Trusts

Unlike with a revocable trust, the grantor of an irrevocable trust cannot change or amend its terms. Any property placed into the trust may only be distributed by the trustee as provided for in the trust document itself.

For instance, the grantor may set up a trust under which they will receive income earned on the trust property, but that bars them from directly accessing the trust funds. This type of irrevocable trust is a popular tool for Medicaid planning.

Testamentary Trusts

As noted above, a testamentary trust is a trust created by a will. Such a trust has no power or effect until the will of the grantor goes through the probate process. (Learn more about what probate entails in another article.)

A testamentary trust will not avoid the need for probate. It also will become a public document when you have passed away. This is because it is a part of the will.

On the plus side, it can be a useful estate planning tool for accomplishing other goals. For instance, you can use a testamentary trust to reduce estate taxes on the death of a spouse or to provide for the care of a child with disabilities.

Supplemental Needs Trusts

Another type of trust is a supplemental needs trust, or special needs trust. It enables the donor to provide for the continuing care of a disabled spouse, child, family member, or friend.

For instance, a loved one with a disability may receive benefits through a public assistance program. If they are the beneficiary of a well-drafted supplemental needs trust, they will also have access to the trust assets. They can then use the trust funds for purposes other than those provided by public benefits programs.

In this way, the beneficiary will not lose eligibility for benefits such as Supplemental Security Income, Medicaid, and low-income housing. You can create a supplemental needs trust for someone during your lifetime or make it part of your will.

Credit Shelter Trusts

Credit shelter trusts are yet another common type of trust. For married couples, a credit shelter trust offers a way to ensure their surviving spouse can take advantage of state and federal estate tax exemptions.

Partner With an Estate Planning Attorney

If you are looking for more information on trusts, connect with a qualified estate planning attorney in your area. They will be familiar with the rules governing the various types of trusts in your state. Whether you want to shield a piece of real estate from creditors or ensure your hard-earned funds will eventually pass to your minor children, your estate planner will be able to find the best trust for your situation.

For further reading on trusts, refer to the following helpful articles: